Market convention is to quote the shape of the UST yield curve by looking at 10Y UST v 2Y UST. Every bond trader and bond trading desk does it and in the institutional fixed income world this is what you quote in conversation about the shape of the yield curve. It’s just how you rap in the bond world.

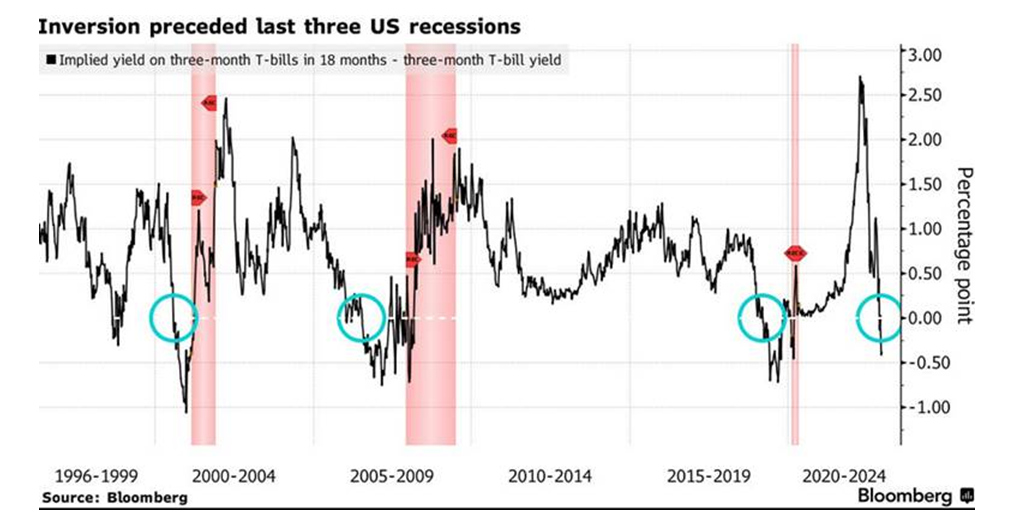

If you really want to know whether the bond market think the Fed is reducing liquidity/jamming on the brakes on the economy it’s very helpful to look at very, very short rates and the difference between implied 3mo T bill rates and actual 3mo T bill rates. The pink shaded areas below are past recessions. Inversion of implied short rates v. actual short rates precede economic recession/contraction.

Does the bond market think we are going to a recession in early 2023? Yes. Do we think we are going to have a recession in early 2023? Yes. Is the equity already braced for an economic recession in early 2023? I think yes. Equity market multiples have already done a big reset and market sentiment has already moved to historic lows. It’s not over yet as volatility will likely persist until the Fed officially pauses – it’s not that far away. Money supply is already cratering, inflation is already coming down across the board, and demand is being destroyed daily via a combination of Fed rates hikes and quantitative tightening (QT). The path forward begins with the Fed changing direction on policy. Maybe not in time for this late December but yes, the Santa Pause is comin’ to town.

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.