The US economy continues to hang in there just fine but inflationary data on many fronts continues to fall and the bond market is pricing in just a 10% probability of a Fed rate hike come September. So, with the Fed near done with rate hikes and Fed chair Powell warming up for his big speech next week in Jackson Hole (“our work here is done”), one would think that the bond futures market would have less gloom…not so.

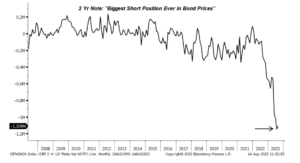

Positioning at the very front end of the UST curve is way off-sides. The last time short interest was this high on 2y UST was…never. The last time I saw positioning this far off-sides was when the world was short the SP500 last October 2022 (FYI equity markets are up about +25% from that occurrence). To put it simply, the bond futures market is not ready for what I think will happen next week at Jackson Hole: a Fed declaration that the war against 2021 COVID related inflation is over.

When so many have bet that 2Y UST yields are headed higher the opposite often/usually/always happens. Economy slower, yields lower.

Risk assets will LOVE short, dated yields going lower. Not like, LOVE. The time to be short 2Y UST was when 2Y UST rates were zero, not 5%. Positioning not consistent with a Fed about to go into extended “pause mode”.

Source: EISI as of August 14, 2023

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.