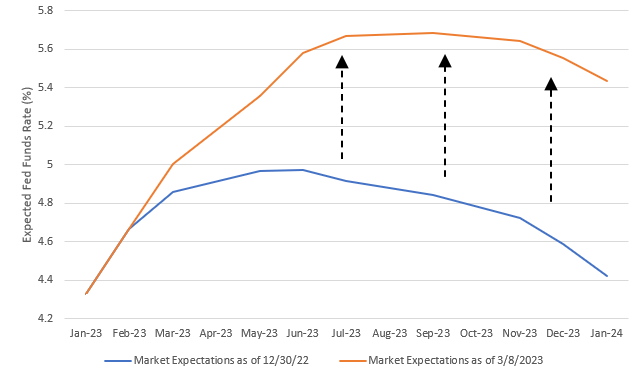

As much as Fed Chair Jerome Powell may claim that the Fed is not trying to push the economy into recession, it is becoming increasingly likely that their fight against inflation will produce that exact result. Following a series of stronger than expected economic data prints over the last couple of months, and Powell’s newly preferred inflation measure (core services excluding shelter) remaining stubbornly elevated, investors have been forced to reassess their expectations concerning the future path of interest rates. Whereas at the beginning of the year investors were expecting the Fed to only hike rates twice in the first half and to cut them once before year-end, investors now see the Fed hiking rates five times in 2023 before cutting them once before year-end. The chart below shows just how much expectations have shifted in just over two months.

A 2023 Dovish Pivot is Getting Priced Out of the Market

Source: Congress Wealth Management, Bloomberg, as of 3/8/2023

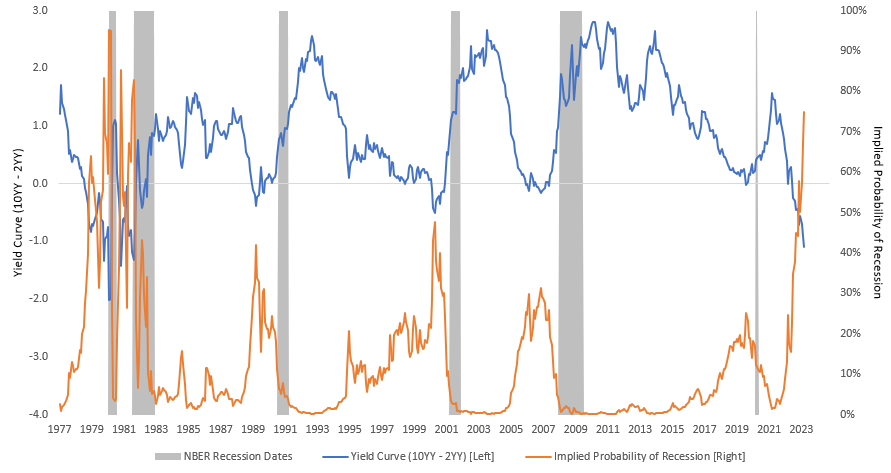

In his recent testimony to Congress, Powell did very little to push back against such a hawkish turn in expectations. This caused the yield curve, calculated as the spread between the 10-year and the 2-year yield, to extend more deeply into negative territory, reaching a level of -108 bps at the time of writing. This is the most inverted the curve has been since 1981, when then Fed Chair Paul Volcker was forced to cause a double-dip recession to combat entrenched double-digit inflation rates. As we have explained in the past, the yield curve has a remarkably strong record in forecasting recessions with 12-to-18-month lead time, and the current historic level of inversion is consistent with a commensurately historic recession probability of 75%. While the yield curve is only one of the components of our proprietary recession probability model, its latest message is consistent with that of the model as a whole: recession risks continue to increase to uncomfortable levels.

The Yield Curve is the Most Inverted Since the Volcker Era

Source: Congress Wealth Management, National Bureau of Economic Research, Bloomberg, as of 3/8/2023

This Friday the Bureau of Labor Statistics will release payrolls data for February, and we will get another clue as to whether the economy continues to defy gravity, or whether some cracks are beginning to form. Given the surprisingly strong momentum with which the economy entered 2023, it is quite possible that the data will keep surprising to the upside for some time still. However, given how hard the Fed keeps slamming on the brakes, a significant slowdown down the road, likely by late this year or early next year, seems all but inevitable.

Sauro Locatelli CFA, FRM™, SCR™

Director of Quantitative Research

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.