Tough to say anything other than this morning’s labor report is indicative of a continued strong labor market and a still ok economy. +260K adds to nonfarm payrolls, led by the private sector. Average hourly earnings +.4% for the month, with both hours worked and hourly wages higher. The favorable market reaction is to the unemployment rate ticking up to 3.7% from 3.5% and the household employment data telling a different story than the gains in the payroll data. Household employment has been stale now for the past 4 months – have to do some more digging here but it looks to be more people working two jobs, not more people working…more to follow. We still have TONS of economic data to come in the next month, but this labor report signals enough ammunition for the Fed to hike 50bps in December. For the Fed to really start thinking and talking about “pausing”, I think it’s going to need the unemployment rate to get to 4%. More labor destruction required, but I think we’re on a path there already.

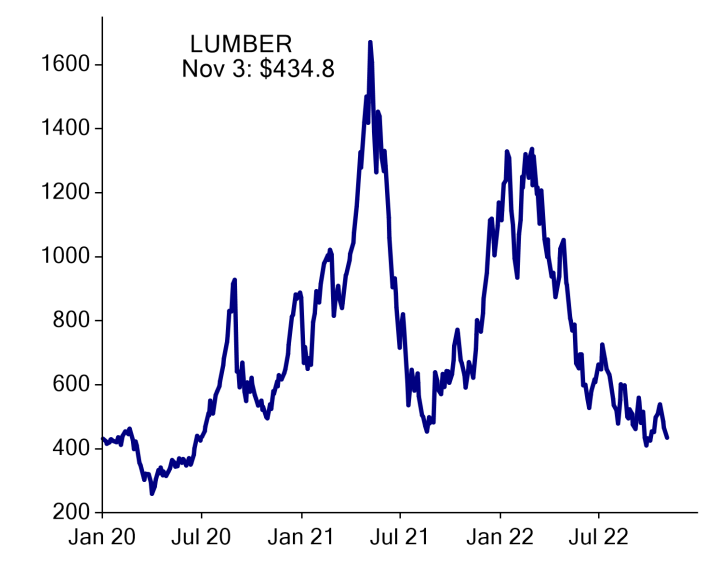

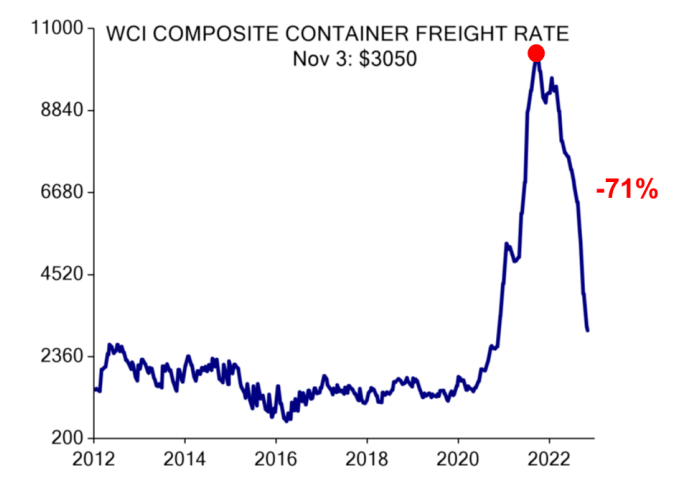

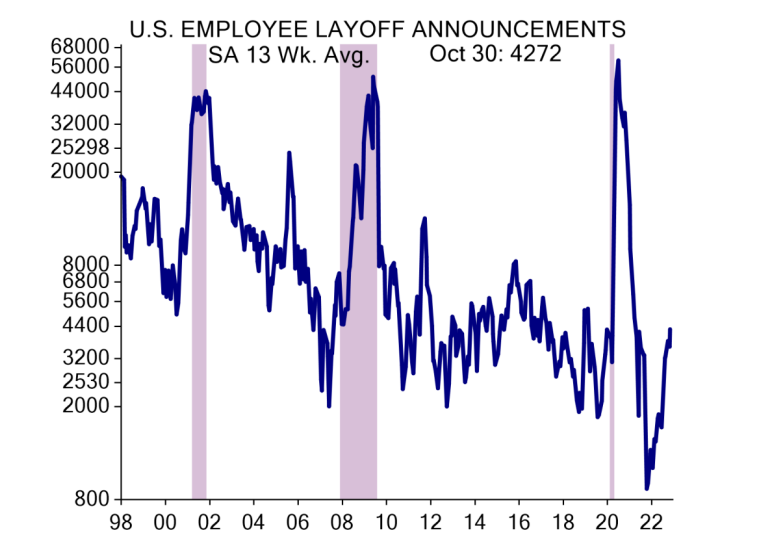

The big picture is that mortgage rates are now +7%, the front end of the yield curve is inverted, and economic demand is falling and falling fast. Lumber prices have collapsed, freight rates have collapsed, and layoff announcements are up a lot. The combination of higher rates, a strong USD, the Fed hiking rates hard and fast, and quantitative tightening now running at $95 billion a month (Fed balance sheet shrinking) is all taking its toll. We printed $3-4 trillion too much stimulus to fight the pandemic and that needs to be consumed by inflation. Much of it already has been. The economy is losing altitude quickly, and while tough talk and perhaps some tough love by Fed chair Powell might work behind the microphone at a press conference, if the Fed isn’t very, very careful here they risk turning a recession into a crisis.

In this market, “bad news” now equals “good news”. We need some “bad news” in order to get the Fed to hit the brakes on hitting the brakes.

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.