As of Friday, November 4th 83.5% of S&P 500 companies have reported Q3 earnings. How did the quarter go, and what have we learned? Let’s look at a few charts.

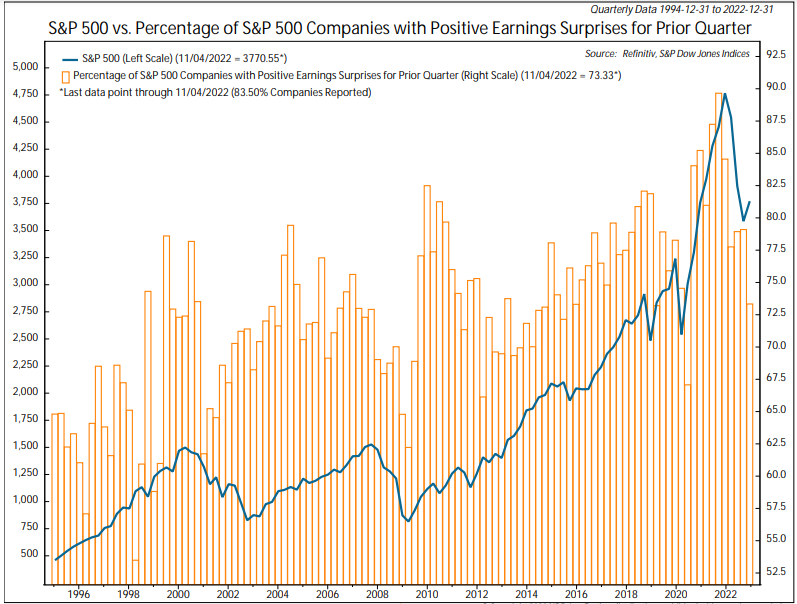

Companies announcing earnings for Q3 2022 had a beat rate of 73% which seems like a solid number. But as you can see in the chart below this is the lowest beat rate since the COVID lows of 2020, and among the lowest beat rates since the end of the financial crisis in 2009. It is also decelerating at a rapid pace from the 90% beat rate at the end of 2021.

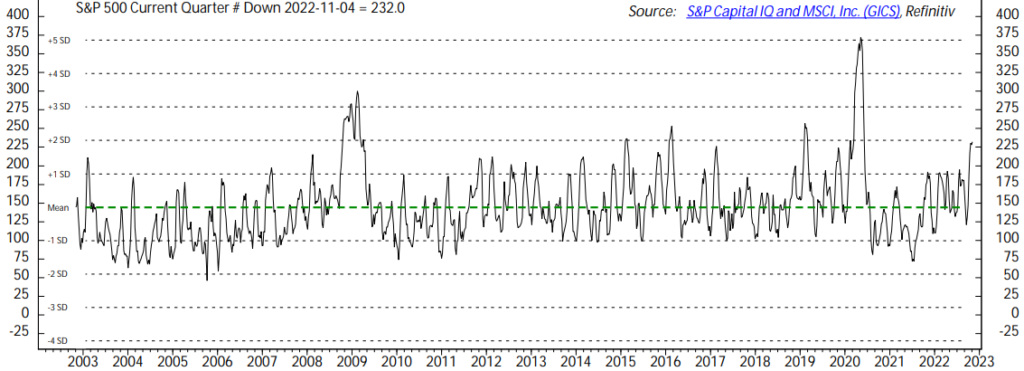

The beat rate comes into more focus when we look at negative earnings revisions for the quarter. 232 companies saw earnings revised lower for Q3 which is much higher than the mean going back to 2003, and on par with the 2016 manufacturing recession and Powell’s 2018 folly. The only periods that saw more negative revisions were COVID and the financial crisis.

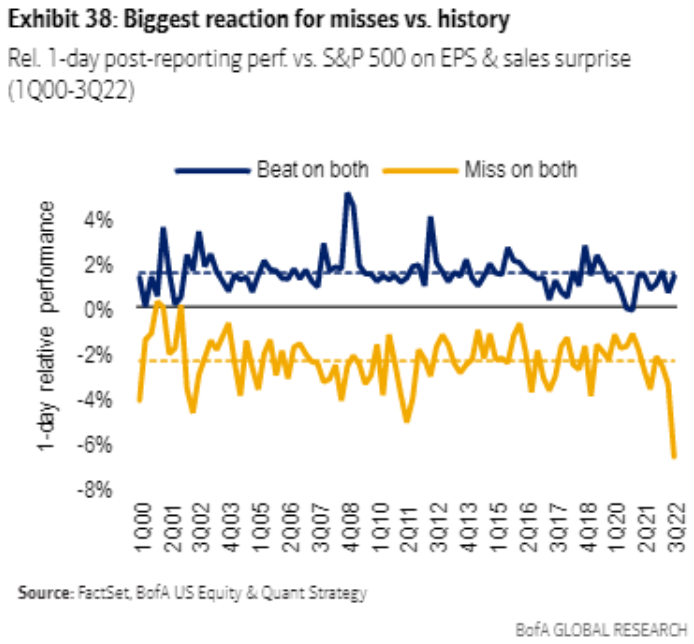

And Mr. Market is certainly picking up on this theme. If you revise lower, and still can’t beat the number, the stock is experiencing the biggest negative reaction going back to 2000.

So, all in all Q3 earnings have been rather weak with a smaller beat rate on top of marked down earnings (not too surprising as economic activity continues to slow). And owning high quality companies that can outperform their estimates has been very important over the last few weeks. More important to investors is what we see for 2023 earnings as this quarter ends.

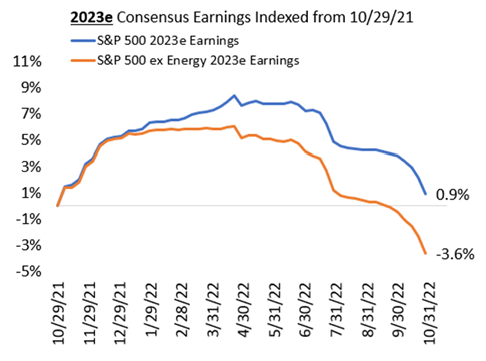

The chart below shows S&P 500 earnings ex. Energy falling about 7% from April 2022 to current (from 105 level to 97.4 level). We have noted previously that in short and shallow recessions earnings typically fall 10-15%. If we are right in that assessment, then earnings should still have more to fall BUT we are closer and closer to that recession being priced.

Sean Dillon, CMT, CFTe

SVP, Investment Strategies

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.