Markets haven’t experienced higher inflation and higher yields in a really long time, but that’s the world we find ourselves in right now.

The Fed and the Market seemed to be on the same page leading up to last December. Both saw rising/persistent inflation and both agreed on the need for higher rates. Back in December, the front end of the yield curve (shorter dated maturities) was pricing in 4 rate hikes for 2022 The Market and the Fed were in agreement on that then. All that quickly changed when inflation accelerated higher AND the Fed kept doing quantitative easing (money printing/bond buying/bigger Fed balance sheet) thru March. Inflation everywhere and a shortage of labor does not need monetary stimulus. Fire does not need fuel. The Market has sent the Fed a direct message that the Fed “didn’t get it” and sent short rates markedly higher.

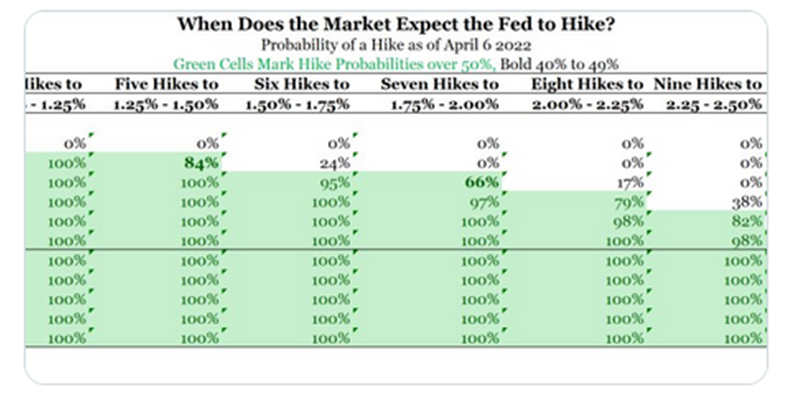

The Fed usually controls the front end of the yield curve. The Market has complete control over it right now. The Market is telling the Fed that they are behind in fighting inflation and that short rates need to go up a lot. The Market is daring the Fed to go faster and do a series of +50bp rate hikes. Back in December four rate hikes were priced in; today the Market is pricing in almost 11 +25bp hikes for FY2022.

What are the implications? Higher rates will slow the economy. An inverted yield curve (short rates > longer rates) will cause a recession about 18 months after such persistently occurs. Right now we are not inverted – mainly due to 10y UST rates rising faster than 2y UST rates. WATCH THE SHAPE OF THE YIELD CURVE. If we get a late 2023 recession, it’s because the Fed went too fast too late and caused such to happen during 2022.

Long rates need to be > short rates. It’s all about rates and always will be. The cost and availability of money and credit drives the economy, investment, and ultimately corporate earnings growth. And earnings drive the direction of the equity market.

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.