There is certainly a lot happening in the financial markets right now. It is more important than ever during times like this to step back and focus on what we do know. And the clearest messenger right now is the bond market.

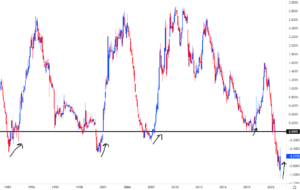

We have discussed the 10-2-year treasury yield curve a lot over the last year. An inverted yield curve, which means the 10-year treasury yields less than a 2-year treasury, is a great pre-condition to a recession. However, it is the “de-inversion” of the yield curve that signals a recession is close to occurring. In the chart below, and indicated by my horribly drawn black arrows, you can see this “de-inversion” occurred before every recession since 1989. Over the last few days the 10-2 yield curve has moved from -1.10% to just -0.5%, which is the bond market telling us that recession is coming.

Source: Bloomberg as of 3/15/23

Why does this occur? It is because the market starts to price in Federal Reserve rate cuts. With the banking issues that have arisen over the last week, we see a dramatic reversal in the Fed Funds rate expectations. The current Fed Funds target rate is 4.75% but the market now expects that rate to be 3.85% by January of next year, or close to 1% lower due to recession expectations. This leads to a drop in the 2 year treasury rate, which has fallen from 5%+ to just 3.8%, and the de-inversion.

Source: Bloomberg as of 3/15/23

We think the bond market has now officially priced in a recession, sooner rather than later. HY credit remains a key area to continue to avoid.

Sean Dillon, CMT, CFTe

SVP, Investment Strategies

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.