The VIX index, frequently referred to as “the Fear index”, is a widely followed measure of market volatility. It is derived from the prices of one-month call and put options on the S&P 500 index, providing us with a real time gauge of market participants’ expected volatility over the near term. The VIX index tends to spike during periods of market turbulence, such as the COVID sell-off in the Spring of 2020 or the Global Financial Crisis of 2008-2009. It then tends to revert back to lower levels as fear subsides and the market settles down. We have previously written about how spikes in the VIX index tend to provide good buying opportunities for stocks. As the old adage goes, “be greedy when others are fearful”. However, by the same token, are low levels of the VIX a good selling opportunities? Should we be concerned about the fact that the VIX has now fallen to the lowest level in over three years?

VIX INDEX

Source: Bloomberg, as of 7/3/2023

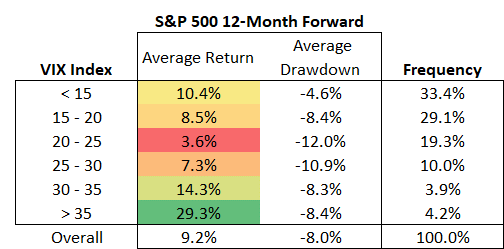

The table below breaks historical values of the VIX index since 1990 into a few different ranges, ranked from the lowest (below 15) to the highest (above 35). For each range, the table reports the average S&P 500 index return over the following 12 months, the average drawdown over the same period, and the frequency of occurrence of each range. From the table, we can make two main observations:

- First, the table confirms that spikes in the VIX provide great buying opportunities. Values of the VIX above 35 are rare, historically occurring just over 4% of the time. However, when they do occur, they are followed by average 12-month forward returns of 29.3%!

- Second, the table disproves the idea that low levels of the VIX should be used as selling opportunities. Values of the VIX below 15 are far more common than values above 35, occurring over 33% of the time. Average returns over the following 12 months come in at a not-so-shabby 10.4%, which is certainly lower than 29.3%, but higher than the overall average of 9.2%. Perhaps more interestingly, these returns come with an average drawdown of just -4.6%, which is nearly half as much as the overall average of -8.0%.

In summary, low levels of the VIX are associated with still-solid forward returns, and these returns are a lot less risky than the ones associated with higher levels of the VIX. History says that investors using the excuse of a low VIX index to get out of stocks may end up spending a lot of time out of the market, potentially missing out on significant gains.

Source: Congress Wealth, Bloomberg, as of 7/3/2023

Sauro Locatelli CFA, FRM™, SCR™

Director of Quantitative Research

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.