“Goods inflation” was the big story of 2020. The pandemic happened, we tried to reopen the economy but factories weren’t open. Lumber prices soared, container ships backed up at West Coast ports, 15-week backlog to get new home furniture. Not enough goods – prices soared.

“Service inflation” was the big story of 2021. Vaccinations happened, people wanted to go out and try to live like they used to live. Let’s be honest: there’s only so long you can spend time at home with your ‘loved ones’. Hotels tough to find, airlines booked solid, tough to get a reservation at your old favorite restaurant. Not enough service labor – prices soared.

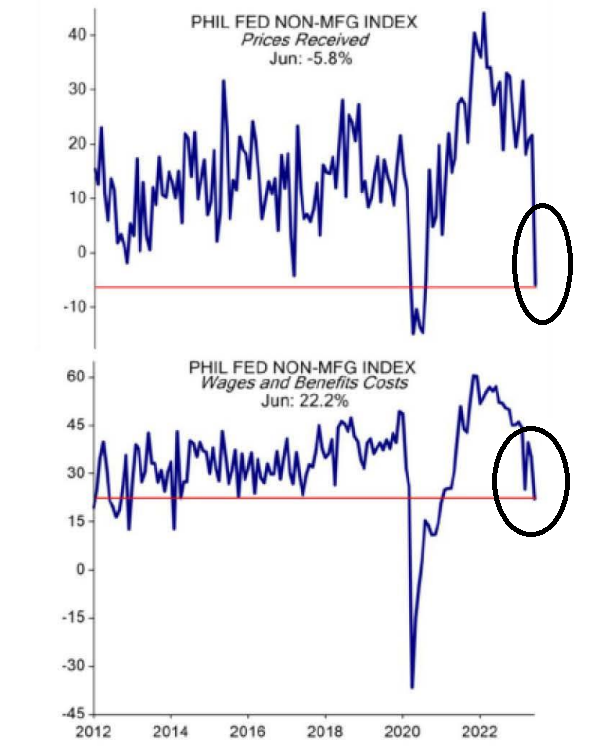

And while the Fed got WAY BEHIND this whole phenomenon, eventually the combination of hiking interest rates at the fastest pace ever AND shrinking their $9 trillion balance sheet takes effect. Eventually the drug works. During 2022, the cost of money went up, financial conditions got tighter, and prices have been and are correcting right on cue. PMI manufacturing prices are materially lower and headed lower. Service inflation, as measured by service prices and service labor, going in the same direction – LOWER. The charts and data agree.

This Powell-led Fed probably hikes 25bps in July to prove their worth but any rate hike after that likely brings into reality the possibility of a hard(er) economic landing in 2024. June wasn’t a Fed “pause”; it was the Fed “Skip”. But if they are not careful, the Fed will find themselves fighting inflation that will be back under < 3% CPI inflation within months. The market won’t like the Fed fighting something that doesn’t exist. To me that feels like late 2018 when Powell hiked but inflation was tame/lame.

Big picture is that inflation is in the rearview mirror. I think the stock market agrees, I think the bond market sort of agrees, commodities agree, I think the USD trend agrees, and I hope Powell and his Fed sees this too.

Source: EISI as of June 27, 2023

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.