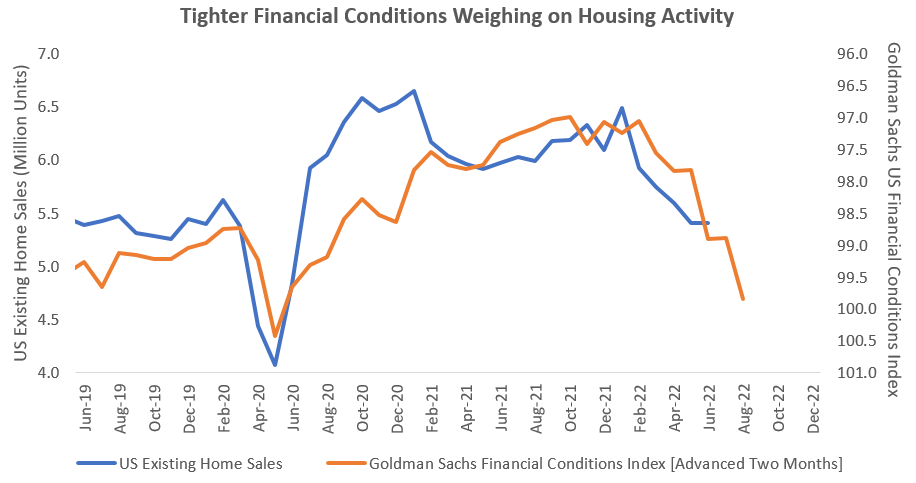

As the latest sign that the economy is slowing down, the once red-hot housing market is starting to sputter. Based on data released this morning, only 5.41 million existing homes were sold in the US in May, which is 3.4% lower than the prior month and 8.6% lower than the same month a year ago. 5.41 million is also the fewest existing homes sold since the first half of 2020, when pandemic-induced lockdowns caused the economy to grind to a halt.

Back then, the Fed quickly came to the rescue by slashing interest rates and flooding the economy with liquidity. Unfortunately, that is unlikely to happen this time around. In fact, Federal Open Market Committee (FOMC) members may be congratulating themselves right now, because this is exactly what they have been trying to accomplish. With inflation running way above the Fed’s target of 2% for much longer than could be considered transitory (at least while keeping a straight face) and no control over supply, the Fed’s only option at this point is to curb demand. They are doing that by hiking rates and removing liquidity from the system, thereby inducing a tightening of financial conditions.

The latest batch of economic data – whether it’s housing, retail sales, industrial production, employment – clearly points to a broad-based slowdown, but the Fed will likely need to keep at it for a while longer before inflation cools down enough for the Fed to declare mission accomplished. Until then, keep your seatbelts fastened.

Sauro Locatelli CFA, FRM™, SCR™

Director of Quantitative Research

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.