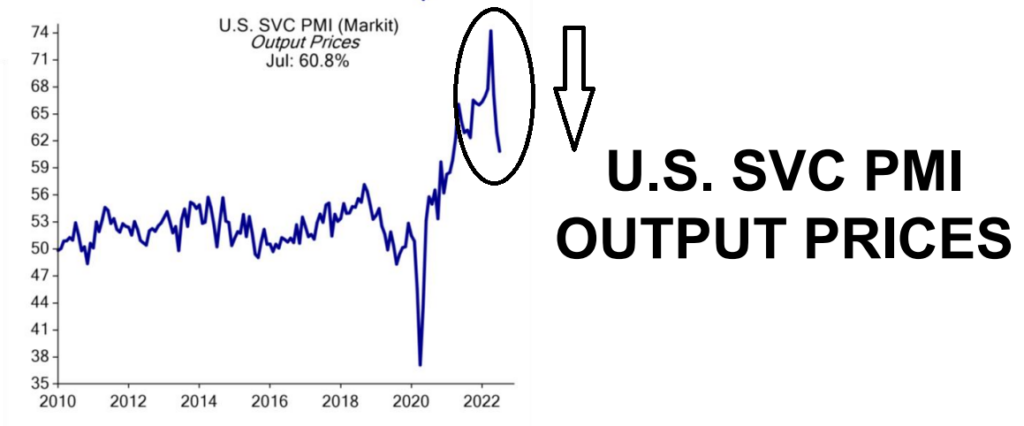

The bond market already has hiked rates to 3%. The Fed is playing catch up but will get there in the coming 3 months. What they do from there will determine whether we get a FY23 recession. If the Fed focuses on backwards data via a rear view mirror they probably will hike 2x too much. If they focus on forward looking data, they will probably see that a lot of demand has already been destroyed, inflation is coming down, and bond yields have stabilized. A lot of commodity prices have rolled over already and have headed lower. Add to that list of lower prices “US service PMI” – a measure of the price of services. Those prices peaked in 1Q and are down sharply since. The reading on this data is usually in the 50s so a reading of 60 is still elevated – but a long way from 74 which is where it was in 1Q22.

The moment of truth in all of this will likely come in late September or early October when the Fed utters the magic phrase: “we’re pausing on rates for now”.

FTF = follow the Fed

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.