All-important CPI inflation data out this morning, and while the market’s reaction has been favorable since 8:30am EST there’s lots to evaluate here. Has the headline CPI inflation number fallen enough to put the Fed in “pause mode” for the summer? The trend of inflation is declining but inflation itself is still elevated – more hikes to come? The housing component of CPI hasn’t fallen enough but all the rental market data says that rents are falling A LOT. And used car prices strangely rose in the past month– breaking an 8 month trend – why? Too many questions, not enough answers. I am on coffee #3 and my head hurts.

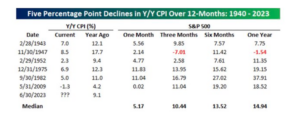

The bigger thing to focus on is this: has substantial progress been made in the Fed’s fight against inflation? The answer is yes. The Fed has taken CPI inflation down from 9% a year ago to roughly 4.3% today. That may not be complete progress but that is substantial progress. And the market agrees. Instead of trying to interpret price data on the fly, another way to think about whether substantial progress has been made is to look to the past. In the past 83 years, there have only been six other times in which CPI inflation data has fallen by at least 5% in a year – we are currently in observation #7.

The data speaks for itself – forward market returns from such substantial progress versus inflation are well above average looking out 6-12 months. #datadontlie

Source: JonesTrading LLC as of June 13, 2023

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.