“Inflation is always and everywhere a monetary phenomenon”

– Nobel Laureate Milton Friedman in speech given in India in 1963

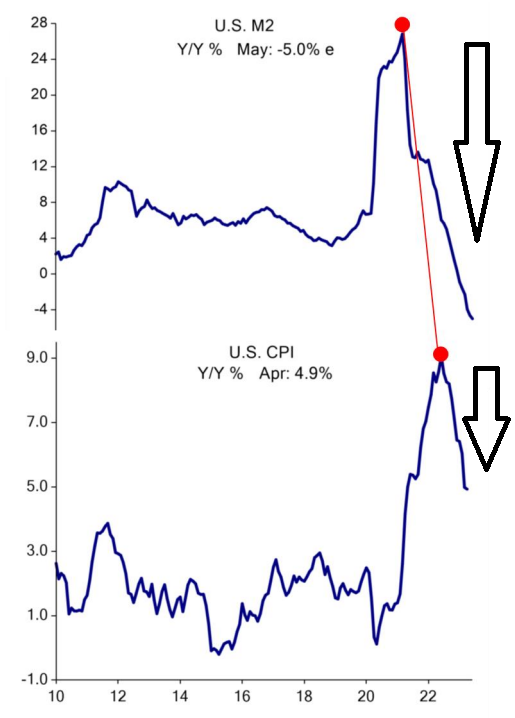

We have discussed before many times that money supply growth drives the direction of inflation. When money supply growth is soaring (M2 in chart below), inflation soon follows. Too much currency chasing the same amount or fewer goods. Inflation 101.

M2 money supply growth grew at 2-5% annually for the past 70 years and then COVID arrived. During the first 24 months of COVID, M2 money supply grew by +45%, record setting money printing. We flooded the system with about $3 trillion too many and inflation (CPI) reacted accordingly. The bad news is that inflation is still elevated. The good news is that money supply growth is now cratering, and inflation will soon follow. The direction of both money supply growth and CPI inflation is headed lower-er.

It’s hard to see an aggressive Fed policy calling for higher rates with a backdrop of a big drop in money supply, a sharply declining pace of CPI inflation, ongoing regional/small banks crisis, and the US economy likely in a recession by Labor Day 2023. I think the Fed is likely done on rate hikes.

FTM = follow the money.

Source: EISI as of May 23, 2023

Richard Barrett

Chief Investment Officer

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.