The latest CPI inflation report was just released this morning, and so far it’s put markets in a very good mood. The details were certainly encouraging with headline inflation flat month over month, and up only 3.2% year over year. Core CPI was only 0.2% higher on the month and 4% YOY, which is the lowest in two years.

The reaction was swift with stock futures jumping and bond yields plunging. This goes to show that as much as the markets HATED high & rising inflation last year, they’re similarly relieved now as it continues to descend the other side of the mountain. From the Fed’s standpoint, this solidifies that there will be no hike in December at a minimum – with rising odds that they’re altogether done now. In fact, the market is now anticipating that their next move will be a quarter-point cut in June of next year.

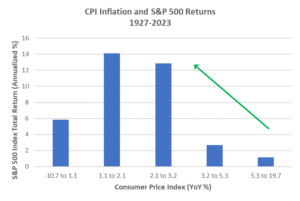

Today’s positive knee-jerk reaction does make sense in the context of the longer-term history of inflation and stocks. If we look at monthly CPI readings since 1927 divided into even quintiles (meaning that 20% of observations are in each), we can see that the S&P 500’s returns are strongest in the 2nd and 3rd quintiles when inflation is positive but low (between 1.1 – 3.2%). CPI first slid back into this “sweet spot” in June when it fell to 3% YOY, after being in either the 4th or 5th quintile since April 2021. Following a brief uptick the last couple of months, today’s report helped to confirm that the downward trajectory into the middle quintile is intact.

Of course, this has nothing to do with other aspects of the economy, earnings, etc., where there are some risks looking ahead. But on its own, inflation is clearly turning from a headwind to a tailwind for stocks as it continues to moderate.

Source: Bloomberg, Bureau of Labor Statistics as of 11/14/23

Carl Noble, CFA®

Senior Vice President of Investments

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.