Another quarter is soon drawing to a close and investors will once again turn their focus to the latest corporate results. With the next round of news on inflation and the Federal Reserve still a few weeks away, earnings announcements will take center stage and help to shed light on how increasing signs of demand destruction in the economy are affecting bottom lines. For most of this year, the resiliency of earnings has been impressive even as the Fed kicked their rate hiking campaign into overdrive. But that has started to change recently as forecasts are finally being marked down.

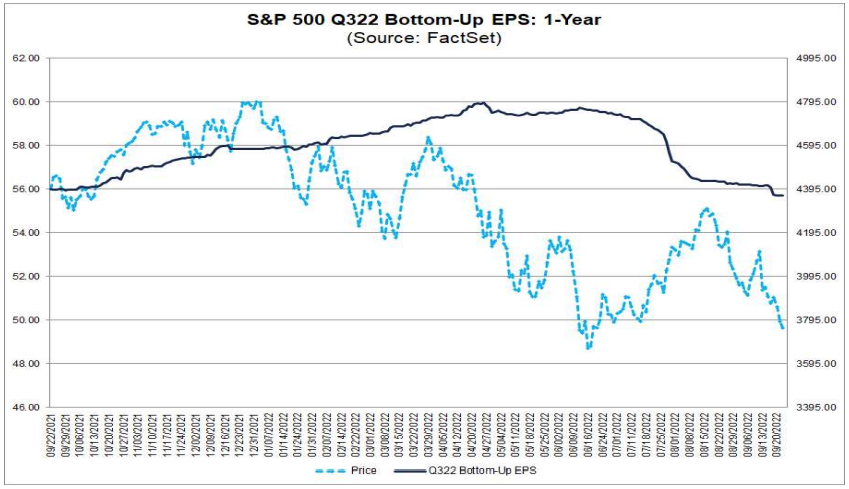

Looking at the journey for the S&P 500’s Q3 estimate it has now made a round trip – starting at $56 back in late 2021, climbing to a high of $60 in the spring, and backing off to just below $56 (dark line on the first chart). If accurate, it would be a small sequential decline from Q2 and at 3.2% would be the slowest annual growth rate since the Q3 2020. Anecdotally, recent warnings from companies like FedEx have helped to put the market on edge about the possibility of further disappointments as results roll in – in particular, will lofty profit margins finally succumb to the ongoing pressure from high inflation & soaring interest rates?

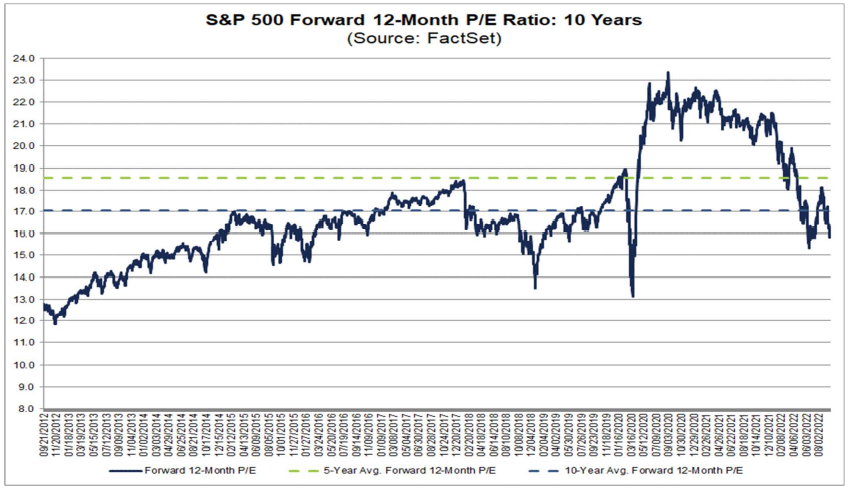

Given the latest bout of volatility, it’s clear that the market isn’t waiting around to find out the extent of earnings damage that’s going to occur from a slowing economy. However, the decline in stocks this year also suggests that an earnings slowdown has been discounted to some degree given the plunge in the P/E ratio, with the current S&P 500 forward P/E multiple of 15.7 slipping further below both the 5- and 10-year averages. In fact, the contraction in the multiple of more than 20% (from 23x earnings to approximately 16x now) is consistent with some of the darkest periods in the last several decades.

“How much is priced in?” is a recurring question on the lips of nearly every investor these days. This earnings season should go a long way in helping to answer that.

Carl Noble, CFA®

Senior Vice President of Investments

Congress Wealth Management LLC (“Congress”) is a registered investment advisor with the U.S. Securities and Exchange Commission (“SEC”). Registration does not imply a certain level of skill or training. For additional information, please visit our website at congresswealth.com or visit the Investment Adviser Public Disclosure website at www.adviserinfo.sec.gov by searching with Congress’ CRD #310873.

This note is provided for informational purposes only. Congress believes this information to be accurate and reliable but does not warrant it as to completeness or accuracy. This note may include candid statements, opinions and/or forecasts, including those regarding investment strategies and economic and market conditions; however, there is no guarantee that such statements, opinions and/or forecasts will prove to be correct. All such expressions of opinions or forecasts are subject to change without notice. Any projections, targets or estimates are forward looking statements and are based on Congress’ research, analysis, and assumption. Due to rapidly changing market conditions and the complexity of investment decisions, supplemental information and other sources may be required to make informed investment decisions based on your individual investment objectives and suitability specifications. This note is not a complete analysis of all material facts respecting any issuer, industry or security or of your investment objectives, parameters, needs or financial situation, and therefore is not a sufficient basis alone on which to base an investment decision. Clients should seek financial advice regarding the appropriateness of investing in any security or investment strategy discussed or recommended in this note. No portion of this note is to be construed as a solicitation to buy or sell a security or the provision of personalized investment, tax or legal advice. Investing entails the risk of loss of principal.

Comments are closed.